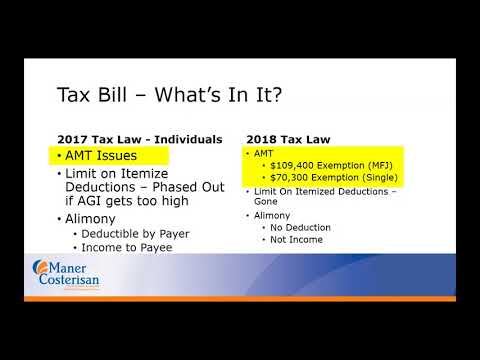

Good morning everybody, welcome to today's webinar on the Tax Cuts and Jobs Act and individual tax update. My name is Matthew Latham, and I'm a senior manager in the tax department at Manor COO Saracen. Today's topic is basically looking at the individual tax impacts of the Tax Act that was passed towards the end of last year. We will take a look at some general impacts, such as rate changes, deduction changes, and dealing with loss carryforwards. We will also discuss state tax changes and impacts that have occurred over the last year. Starting off on December 22nd, 2017, President Trump signed the Tax Cuts and Jobs Act. Most of the provisions went into effect as of January 1st of this year. However, there were some exceptions dealing with mortgage debt and depreciation for those with businesses that flow to their 1040. An important distinction to note is that the individual provisions generally expire after 2025, whereas the corporate provisions, such as the corporate tax rate cuts, do not expire. A lot was put into this bill to try to make filing your 1040 a little easier. However, there were some curveballs included that we will have to dig into. Some clear-cut changes include the reduction of individual tax rates, minimizing the effect of the alternative minimum tax, and changing the individual health insurance mandate after 2018. There have also been changes to standard deductions, exemptions, and itemized deductions. One significant change is that the estate, gift, and generation-skipping tax exemptions were doubled from five million to ten million. For business owners, there were changes as well, especially regarding the 199A deduction. We held a webinar last month solely focused on this deduction, as there is a lot to understand. We will briefly touch on it today, but we won't go into too...

Award-winning PDF software

Video instructions and help with filling out and completing Where Form 2350 Update