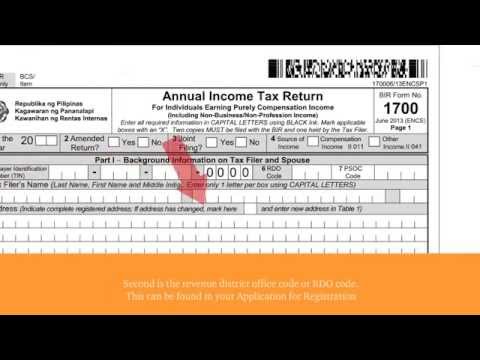

The applicable tax return for an individual earning purely compensation income is the BIR Form 1700. The latest version of this form was released in January. The revised form now has four pages and is divided into five parts. Parts 1, 2, and 3 are on page 1, providing an overview of yourself and your tax liability for the year. Part 1 focuses on you and your spouse. Please note that there is certain critical information you need to provide on this page, such as your Philippine tax identification number (TIN) and the revenue district office code (RDO code). Your TIN can be found on your TIN card, while the RDO code can be found in your application for registration or verified directly with the VAR taxpayer assistance division. Part 2 is a summary of your final tax liability and tax credits for the year. The entries for this portion should be lifted from the computation of your tax liability in part 4. Thus, it is advisable to accomplish part 4 first before completing part 2. Part 3 details your tax payment, including the amount you need to pay upon filing your return and the mode of payment. Part 4 is on page 2 and details the computation of your tax payable. To complete this part, you need to summarize all your earnings during the calendar year, including your gross compensation income and the corresponding taxes withheld by your employer. Make sure to take advantage of allowable deductions and exclusions for employees, such as the 30,000 pesos exception, 13th month pay, bonuses, mandatory contributions, and de minimis benefits. Check the applicable items and indicate them accordingly. As an individual taxpayer, you may also be eligible to claim basic personal exemptions and additional exemptions for qualified dependent children. The applicable amounts...

Award-winning PDF software

Video instructions and help with filling out and completing Form 2350 Filing